A Home does not produce cash-flow, it demands it.

You cannot sell pieces of your Italian marble floor to pay for groceries.

Key Takeaways:

- Taking the maximum mortgage the bank will give you for a primary residence will leave you financially fragile.

- Maintenance and property taxes typically costs 2-4% of the home value annually.

- To access the wealth in your home, you must either sell it (you are left homeless) or borrow against it with a Home Equity Line of Credit “HELOC”), creating a new monthly liability.

- Selling costs 6-10% of the home value (agent fees, closing costs, transfer taxes), destroying a significant part of the returns upon exit.

- People underestimate the emotional cost of downsizing in their golden years. Moving from a 3 bedroom home to a 1 bedroom condo feels like a loss, not a victory.

Invert, Always Invert

There is a problem of human misjudgment I see everywhere:

People look at their primary residence and see a retirement plan.

If I wanted a life of mediocre returns and full of stress, here is what I would do:

I would take all my liquidity, leverage it 4:1 (20% downpayment and borrow the remaining 80%), put it into a single asset that cannot be sold in pieces, requires constant maintenance, and generates no cash flow.

This is exactly what a personal residence is – yet, the world is convinced it is the holy grail of wealth.

Home Rich, Cash Poor

On paper, households look richer than ever: the median net worth of those aged 35-44 stands at $135K and rising to $247K in those aged 45-54.

However, there is an ominous truth behind these figures:

The composition of this wealth is overwhelmingly concentrated in two inaccessible silos: residential real estate and retirement accounts.

For the median household, home equity represents between 60% to 80% of net worth, while liquid assets (cash, checking, savings) represent less than 5% of the portfolio.

5% of $135K is less than $7,000.

As of Q1 2025, the average credit card debt in the U.S. is $6K and a staggering $24K in auto loans, according to Experian.

In other words, most households are dependent on living paycheck to paycheck to meet their monthly financial obligations and are one medical bill away from taking on more debt, digging themselves deeper into the hole.

Because the drywalls of your $500K home will not pay the hospital bills.

To pay for bills, you need cashflow.

Your home does not generate cashflows.

In fact, it requires cashflows to maintain it.

The Real Opportunity Cost

When you buy a house, every dollar trapped in your home’s equity is a dollar that is not working for you in great businesses (Microsoft, Apple, Costco, etc.).

Historically, real estate barely tracks inflation, while the stock market has outperformed by orders of magnitude.

You see, true wealth is created not in the buying or selling, but in the waiting.

In real estate, “waiting” costs you money (property taxes, insurance, maintenance, etc.).

In the stock market, “waiting” pays you dividends.

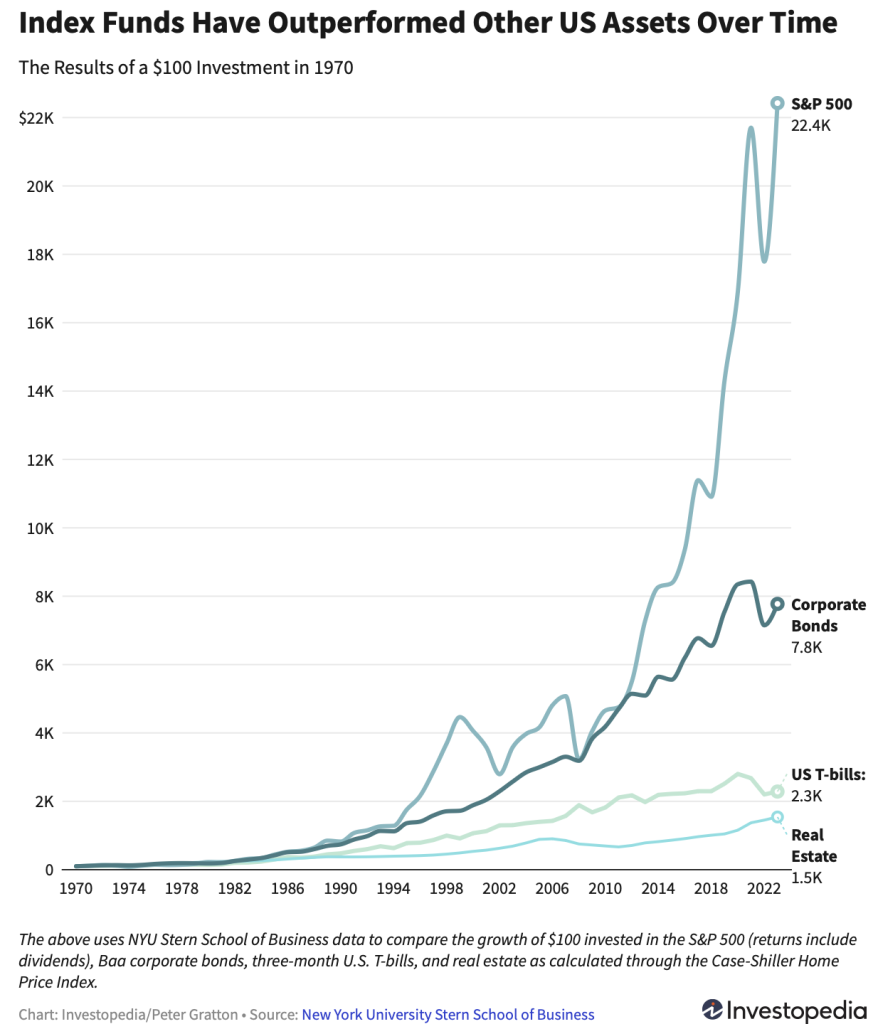

You do not have to believe me, but here are the hard facts:

Source: New York University Stern School of Business via Investopedia.

Basically, the NYU Stern shows that $100 invested in Real Estate back in 1970, would be worth $1,500 in 2023 (a 15x return or 5.24% CAGR “Compounded Annual Growth Rate”) over a period of 53 years.

In contrast, those $100 invested in the S&P500 (the stock market), would be worth $22,400 – a 224x return or 10.75% CAGR.

| Year | Real Estate | S&P500 |

| 1970 | $100 | $100 |

| 2000 | $536 | $4,100 |

| 2023 | $1,500 | $22,400 |

A picture is worth a thousand words.

A home is where you rest. The stock market is where you grow.

The Hidden Friction (Carry Costs)

People ignore friction. It is psychologically easier to deny it.

They will say they bought a house for $500,000 and sold it for $800,000 – “I made $300,000!” they say.

But they conveniently forget:

- The 2-5% closing costs paid at the time of purchase.

- The interest paid to the bank over 10 years.

- The 1-2% property tax and another 1-2% maintenance costs paid yearly.

- The 6% agent fee when they sold.

Subtract all this friction and the real returns are even lower than the one showed in the previous graph.

Putting the same down payment into a low-cost S&P 500 index fund like “VOO” would have most likely provided much higher returns, less fees (“VOO” has an expense ratio of 0.03%), liquidity (you can pretty much buy and sell shares of this ETF anytime) and with zero leaky faucets to fix.

So, are you saying I should Never Buy a Home?

No. We can all agree that buying your own home may improve your quality of life in ways stocks cannot buy: the sense of belonging, memories created with your spouse and kids, etc.

But – there is a gap between this and being asinine.

Remember, the secret to exceptional wealth is consistently avoiding stupidity for a long period of time.

And what does stupidity look like in this case?

Taking the maximum mortgage the bank offers you.

It’s psychological, many homeowners do not buy the house that fits their needs, but the one that signals status.

They buy the biggest house their bank will lent them money for, in turn increasing the amount of taxes, maintenance and utility costs, draining the capital that could have been used to invest in productive assets.

People will complain investing $100 a month in the stock market is out of their possibilities but have no problem buying on credit the latest iPhone every year.

And don’t even get me started on car loans.

Conclusion

There is nothing wrong in buying a home that will really improve your quality of life in a material, psychological or emotional way.

But buying more home than you should will make you dependent on a paycheck to meet the monthly payments, leaving you financially fragile.

When you are financially fragile, you lose the freedom to choose wisely, you stop making decisions based on logic and start making decision based on scarcity.

And scarcity is a terrible advisor, it pushes you into situations you hate, with people you don’t respect for outcomes that barely move your life forward.

Because when you live paycheck to paycheck or barely keep your head above water, you accept deals you know are bad.

You take jobs that drain the life out of you because you need the paycheck.

You attach to people that exploit you because you cannot afford the luxury of saying “No”.

You compromise on ethics, dignity and long term vision because the threat of the short term feels too urgent.

The truly wealthy people follow the same pattern:

- They buy modest homes relative to their income

- They avoid lifestyle inflation like the plague

- They save aggressively and invest relentlessly

- And they keep their living costs predictable

This is the “magic formula” that everyone seem to walk over and miss.

Wealth comes by endurance, not brilliance.

And endurance means consistently avoiding stupidity for long periods of time, while you keep saving and investing in productive assets.

Stay consistent,

– My CEO Lifestyle.

Disclaimer:

The content provided on My CEO Lifestyle is for informational and educational purposes only and should not be construed as professional financial advice. I am not a financial advisor, and you should always do your own research or consult with a qualified financial professional before making any investment decisions. Past performance is not indicative of future results.

Leave a Reply