If you want to retire before 65, saving 20% of your take-home pay won’t be enough.

Key Takeaways:

- Save and invest 20% if you are comfortable retiring at 65 years old (budgeting)

- Boost it to 40% if you want to retire early (wealth management)

- Housing, transportation and wants cannot exceed 60% of your expenses

- Increasing your income is important. Avoiding lifestyle inflation is critical.

- Financial freedom is 90% behavior and 10% math.

From Budgeting → Capital Allocation.

Depending on where you are in life and your monetary goals, personal finance can be divided in two stages:

a. The management of scarcity, widely recognized as “budgeting.”

b. The management of surplus, often termed “wealth management.”

For most people with daily economic constraints, the traditional 50/30/20 rule—spending 50% of income to needs, 30% to wants, and 20% to savings — can work to have solvency and debt elimination (this is budgeting).

If you stay out of debt, this guideline will allow you to retire at 65 and have a modest lifestyle (assuming a full 40-years of accumulation).

But you want to retire before 65. That’s why you are here.

You want to be able to afford to say “No” to a boss and start saying “Yes” to doing more of what you love in life – and so do I.

But to this achieve this, the conventional model is mathematically insufficient.

And there is no way around it: you need to reach a crossover point where your investments generate as much or more cash to fund your lifestyle.

If you need $3,000 a month to cover your expenses, your investments must generate at least that amount in passive income. That is the price of freedom—the point where you never have to accept work that does not align with your values.

“This sounds complicated”. – It is not.

“Okay, but it does sound like it will take some time”. – It will.

Here is the good news: how much you make is not as important as how much you save.

And how much you save is determined by behavior—take a surgeon making $450k a year: if he needs $500k just to sustain a pretentious lifestyle, he is actually broke—living paycheck to paycheck and one step away from disaster.

Conversely, someone who makes $100K and saves $35K consistently is buying freedom. The freedom to quit a job, the freedom of having the bills covered, the freedom to sleep at night.

Yes, making more money helps—but without the right financial behavior, it is like driving a Ferrari at 160mph (high income) without a steering wheel (healthy financial habits), you end up crashing at high speed.

By now, you may sense that someone who saves 0% of their income can never retire, as they have zero accumulated capital and a consumption requirement equal to 100% of their income — they must work perpetually only to break even with expenses.

Instead, if someone were to save 100% of their income, they could retire immediately, as their living expenses would be zero (assuming this is possible).

Between these two extremes lies the curve of financial independence.

At a 10% savings rate, it will take you 42 years to be financially independent (assuming a 7% return after inflation) — this aligns with the “work until death” model.

Doubling the savings rate to 20% does not merely halve the time, it reduces it to roughly 31 years.

Non-linear impact of Savings Rate on Time to Financial Independence*.

*Assuming the Portfolio starts at 0$ and earns a 7% after inflation return, targeting a 4% Withdrawal Rate.

| Guidance | Savings Rate (of net income) | Implied Spending | Years to Retirement |

|---|---|---|---|

| Budgeting | 10% | 90% | 41.7 |

| 20% | 80% | 30.7 | |

| Middle Zone | 30% | 70% | 24 |

| Capital Allocation | 40% | 60% | 19 |

| 50% | 50% | 15 | |

| 60% | 40% | 11.4 | |

| 70% | 30% | 8.3 | |

| 80% | 20% | 5.4 |

You can simulate different retirement scenarios here.

If you started working at 25 and saved 30%, you could be looking to retire just before you turn 50.

Personally, this timeline works for me.

But someone looking to be “off the hook” before 40 would need to have a more aggressive savings rate of around 50%.

All these estimates assume a 7% real return and a yearly withdrawal of 4%, with a high probability of not depleting the capital over a 30-year period.

How Much Do You Really Need? The Freedom Number

To support this withdrawal rate, you should accumulate 25 times your annual expenses, known as the “Freedom Number”.

Freedom Number = Annual Spending x 25

Notice the leverage effect in place here — every $100 removed from the monthly budget reduces the annual spending by $1,200 and this lowers the required portfolio balance to retire by $30,000 ($1,200 x 25).

If you spend $40,000 per year, your freedom number is $1,000,000.

Structural Expenditure Analysis: The “Big Three”

Say you want to retire in your 40’s — as we just saw, you would need to save roughly 40% of your net income, assuming you started working at age 25.

By this imperative, cutting the “matcha lattes” and “avocado toasts” will not be enough.

Instead, we should look into the “Big Three” pillars of the budget: Housing, Transportation and Wants, which typically consume 70% or more of the average household’s income.

Where Does Housing Costs Stand in 2025?

Housing is the largest single line item expense and will set the baseline of how much wealth you will accumulate during your life—it is a massive and relentless multi-decade obligation.

Overextend yourself on a mortgage or rent and you can say goodbye to a wealthy future, as discussed in this post.

According to the latest Q2 2025 Cost of Housing Index (“CHI”) elaborated by the National Association of Home Builders (NAHB) and Wells Fargo, the average mortgage payment represents 36% of a typical household gross income of $104,100.

$104,100 gross income translates to roughly $75,000 after tax (net income).

So, the real mortgage payment typically consumes 45% of the net income.

For reference, it should not exceed 15%(3 times less) if the goal is to achieve a savings rate of 40-50%.

How to align housing costs to a reasonable Financial Independence Budget?

The obvious answer is avoid buying more house than you can afford and do not let the bank decide how much you borrow for the house.

Banks make profits on the interest of the mortgage, the more you borrow, the more they make. Their interests are not aligned to your interests.

Also, here are a couple of options worth considering to minimize the impact a mortgage has on our budget:

a. “House-hacking”: if the home has rentable space, you may benefit from this in two ways:

- Cost Offset: the rental income you obtain helps you offset the mortgage payments. In the best case scenario, this income will completely cover the mortgage or even generate positive cashflow. But if you cannot, any reduction of your monthly payments counts.

- Tax Efficiency: if you do not rent out any space, you can only deduct the interest on the mortgage and property taxes (subject to limits). But when you do rent out part of your property to someone, you are a landlord. And this means you can now depreciate the rented portion of the building, deduct repairs, maintenance and utilities as business expenses.

b. Geo-Arbitrage Renting: for those able to do remote work and willing to stick to renting, “Geo-Arbitrage” can offer a powerful option. This involves earning income from a high-cost-of-living (HCOL) economy while residing in a low-cost-of-living (LCOL) area.

The EPI Family Budget Calculator reveals that housing costs can vary by over 300% between metro areas.

Let’s be clear, buying a home is one of the most emotional purchases we can make in life.

And when emotions get in the way, we make rash decisions without thinking if we can afford it or the consequences down the road.

Most people will not abide by this cap on their mortgage — society will constantly push you to catch up with the Joneses to get the approval from people who have no impact in your life.

But ego and the need to signal success will convince the unprepared any day.

However, If you belong to that minority who understands that a house is not a growth investment and should only provide shelter and create memories with your family and invest the difference, congratulations — this behavioral trait indicates that wealth and anticipated freedom are almost inevitable consequences from your actions.

In my case, I do not own a house.

Even if my income is in the top 10% in one of the wealthiest countries in the world, I understand that if “I live like none else today, I will be able to live like none else tomorrow”, as Dave Ramsey would say.

What About Transportation Costs in 2025

Transportation is the second largest destroyer of wealth for the middle class (excluding university or college for the kids) — the average monthly payment for new cars in Q3 2025 reached a new high of $748 for an astonishing loan term of 69 months and interest rate of 6.56%.

This represents around 12% of the monthly net income and keeps borrowers in a perpetual cycle of debt on a depreciating asset.

How to align transportation costs to a reasonable Financial Independence Budget?

If you want to move from a scarcity (budgeting) to a financial independence approach (wealth management), this expense must be capped aggressively.

A good rule of thumb is to limit the cost of the vehicle to 1/10 of the gross household income.

This means, a reasonable car for the typical family making $104,000 a year should not exceed $10,400 — and yes, this likely means buying a used car but remember that a car is meant to take you from point A to point B, that’s it.

A car is not an investment — in fact, it is a depreciating asset from the moment you drive it out of the dealership. Treat it as such.

The best way to buy a car is cash — get a reliable used car, pay cash in full and avoid taking a loan.

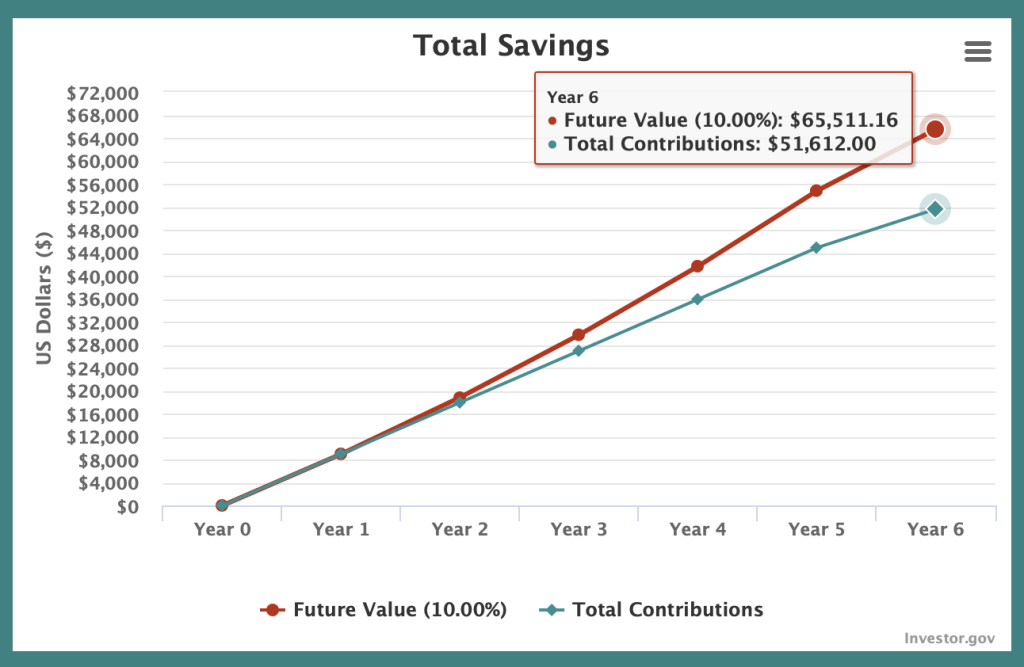

People miss the full cost of buying a car, it is not only the principal and interest paid, but the opportunity cost: $748 invested monthly for 69 months (roughly 6 years) at an interest of 10% (the historic nominal returns of the S&P500), compounds to $65,500.

Source: U.S. Securities and Exchange Commission

So, you have 2 options:

- Option A: Borrow and pay almost $52,000 for a car worth $42,000 that will be worth $12,600 in 6 years.

- Option B: Invest the monthly $748 installments for 6 years at 10% nominal interest (the historic S&P 500 returns), and end up with almost $66,000.

The behavior you choose when buying a car will have an impact on your net worth of more than $50,000.

Cost of Opportunity = $66,000 (Path B)−$12,600 (Path A)= $53,400

Not convinced? The same payment of $748 invested monthly during 40 years turns into $2.3 million at a return of 8%.

Less than $360k of those $2.3 million would be your contributions — a profit of $2 million.

And the last piece of the puzzle: Wants

The latest data provided by the U.S. Bureau of Labor Statistics indicate that people spend almost 17% of net income on discretionary expenses.

While this percentage is lower than what the conventional rule allows (30% to wants), notice how housing (45%), transportation (12%) and wants (17%) add up to almost 75% of the net income.

Needless to say, the average household spends too much on these 3 pillars.

Now, I am not saying that you should eat rice and beans and beans and rice (again, quoting our beloved Dave Ramsey) — at least, not if you are not in debt.

It is important to enjoy the little pleasures of life too, just make sure your Wants do not get out of hand.

In fact, I propose that you change the order of how you spend your salary from:

Pay Housing -> Pay Transportation -> Spend on Wants -> Save Whatever left

To:

Pay Housing -> Pay Transportation -> Save from 30% to 50% -> Spend on Wants

Folks, this is the only way to achieve freedom before 65. The more you save and invest, the more time and options you are buying for your future-self, there is no way around it.

Yes, it is possible with a little organization and will to make some sacrifices – a higher income will definitely help in giving more margin but the behavior and allocation is what will bring you across the line.

I consistently invest 50% of my salary and 90% of my bonus.

Meanwhile, people in my industry spend theirs on champagne, bigger houses, and cars, chasing social validation.

It is an emotional battle because society applauds the spender, not the saver; you get compliments on a new Porsche, never on your index funds.

But the payoff is worth the silence. My portfolio is now compounding faster than my salary is growing.

Every year, my passive income climb closer to my 9 to 5 paycheck.

Soon, it will hit that crossover point.

When that moment arrives, this capital will effectively be more productive than I am—granting me the ultimate luxury of only doing work that aligns with my values.

That is true wealth. Everything else is consumption.

We have covered the why—now let’s handle the how.

In Part 2, we will build a tactical roadmap for anyone starting from scratch. We will break down how to dismantle debt, calculate your safety net, and finally, where to deploy your capital so it starts working for you.

Thanks for reading and see you soon.

– My CEO Lifestyle.

Disclaimer:

The content provided on My CEO Lifestyle is for informational and educational purposes only and should not be construed as professional financial advice. I am not a financial advisor, and you should always do your own research or consult with a qualified financial professional before making any investment decisions. Past performance is not indicative of future results.

Leave a Reply